Monopoly

‘Mono’ means single and ‘poly’ means seller. The term monopoly refers to a market in which a single firm controls the whole supply of a particular product which has no close substitutes. Monopoly emerges in firms such as transport, water, and electricity supply, etc.

1. Single person or a firm: A single person or a firm controls the total supply of the commodity. There will be no competition for the monopoly firm. The monopolist firm is the only firm in the whole industry.

2. No close substitute: The goods sold by the monopolist shall not have close substitutes. Even if the price of the monopoly product increases, people will not go for substitutes. For example, if the price of an electric bulb increases slightly, consumers will not switch to kerosene lamps.

3. Large number of Buyers: Under monopoly, there may be a large number of buyers in the market who compete among themselves.

4. Price Maker: Since the monopolist controls the whole supply of a commodity, they are a price-maker, and they can alter the price.

5. Supply and Price: The monopolist can fix either the supply or the price. They cannot fix both. If they charge a very high price, they can sell a small amount. If they want to sell more, they have to charge a low price. They cannot sell as much as they wish for any price they please.

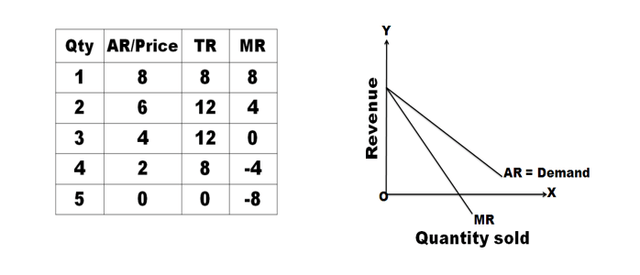

6. Downward Sloping Demand Curve: The demand curve (average revenue curve) of a monopolist slopes downward from left to right. It means that they can sell more only by lowering the price.

Monopoly refers to a market situation where there is only one seller. They have complete control over the supply of a commodity and are therefore in a position to fix any price. Under monopoly, there is no distinction between a firm and an industry because the entire industry consists of a single firm.

Being the sole producer, the monopolist has complete control over the supply of the commodity. They also have the power to influence the market price. They can raise the price by reducing their output and lower the price by increasing their output. Thus, they are a price-maker. They can fix the price to their maximum advantage. However, they cannot fix both the supply and the price simultaneously. They can do one thing at a time. If they fix the price, their output will be determined by the market demand for their commodity. On the other hand, if they fix the output to be sold, the market will determine the price for the commodity. Thus, their decision to fix either the price or the output is determined by the market demand.

The market demand curve of the monopolist (the average revenue curve) is downward sloping. Its corresponding marginal revenue curve is also downward sloping but lies below the average revenue curve. The monopolist faces a down-sloping demand curve because to sell more output, they must reduce the price of their product. The firm’s demand curve and the industry’s demand curve are one and the same. The average cost and marginal cost curves are U-shaped curves. Marginal cost falls and rises steeply compared to average cost. Under monopoly, the demand curve is the average revenue curve.

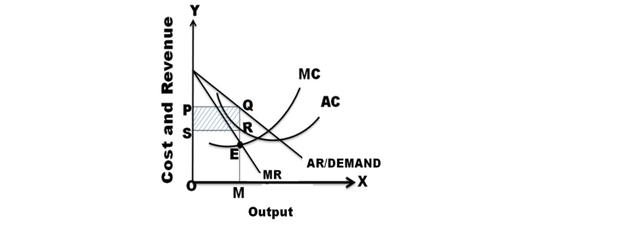

The monopolistic firm attains equilibrium when its marginal cost becomes equal to the marginal revenue. The monopolist always desires to make maximum profits. They make maximum profits when MC=MR. They do not increase their output if their revenue exceeds their costs. But when the costs exceed the revenue, the monopolist firm incurs losses. Hence, the monopolist curtails their production. They produce up to that point where marginal cost is equal to the marginal revenue (MR=MC). Thus, this point is called the equilibrium point. The price-output determination under monopoly may be explained with the help of a diagram.

In the diagram, the quantity supplied or demanded is shown along the X-axis. The cost or revenue is shown along the Y-axis. AC and MC are the average cost and marginal cost curves, respectively. AR and MR curves slope downwards from left to right. AC and MC are U-shaped curves. The monopolistic firm attains equilibrium when its marginal cost is equal to marginal revenue (MC=MR). Under monopoly, the MC curve may cut the MR curve from below or from the side. In the diagram, the above condition is satisfied at point E. At point E, MC=MR. The firm is in equilibrium. The equilibrium output is OM. Up to OM output, MR is greater than MC and beyond OM, MR is less than MC. Therefore, the monopolist will be in equilibrium at output OM where MR=MC and profits are maximized.

The above diagram:

Average revenue = MQ or OP

Average cost = MR

Profit per unit = Average Revenue – Average Cost = MQ – MR = QR

Total Profit = QR x SR = PQRS

If AR > AC; Abnormal or super normal profits.

If AR = AC; Normal Profit

If AR < AC; Loss