Monopolistic Competition

Perfect competition and pure monopoly are rare phenomena in the real world. Instead, almost every market seems to exhibit characteristics of both perfect competition and monopoly. Hence, in the real world, it is the state of imperfect competition lying between these two extreme limits that work. Edward. H. Chamberlain developed the theory of monopolistic competition, which presents a more realistic picture of the actual market structure and the nature of competition.

The important characteristics of monopolistic competition are:

1. Existence of Many Firms: The industry consists of a large number of sellers, each one of whom does not feel dependent upon others. Every firm acts independently without bothering about the reactions of its rivals. The size is so large that an individual firm has only a relatively small part in the total market, so that each firm has very limited control over the price of the product. As the number is relatively large, it is difficult for these firms to determine their price-output policies without considering the possible reactions of the rival firms. A monopolistically competitive firm follows an independent price policy.

2. Product Differentiation: Product differentiation is the essential feature of monopolistic competition. Products can be differentiated by means of unique facilities, advertising, brand loyalty, packing, pricing, terms of credit, superior maintenance service, convenient location, and so on. Through heavy advertisement budgets, Pepsi and Coca-Cola make it very expensive for a third competitor to enter the cola market on such a big scale. The following examples illustrate how firms differentiate themselves from others in a monopolistic environment.

- In the hotel industry, some hotels have spacious swimming pools, gyms, cultural programs, etc. Customers who value these facilities don’t bother about price changes.

- Colleges that provide the best infrastructure and placements in various reputed companies have demand from the student community irrespective of an increase in tuition fees.

- Cell phones with unique features have demand from the public even if prices increase.

3. Large Number of Buyers: There are a large number of buyers in the market. However, buyers have their own brand preferences. So, the sellers are able to exercise a certain degree of monopoly over them. Each seller has to plan various incentive schemes to retain the customers who patronize their products.

4. Free Entry and Exit of Firms: As in perfect competition, in monopolistic competition too, there is freedom of entry and exit. There are no barriers as found under monopoly.

5. Selling Costs: Since the products are close substitutes, much effort is needed to retain existing consumers and to create new demand. So, each firm has to spend a lot on selling costs, which include costs on advertising and other sales promotion activities.

6. Imperfect Knowledge: Imperfect knowledge about the product leads to monopolistic competition. If buyers are fully aware of the quality of the product, they cannot be influenced much by advertisement or other sales promotion techniques.

7. The Group: Under perfect competition, the term industry refers to all collection of firms producing a homogeneous product. But under monopolistic competition, the products of various firms are not identical though they are close substitutes.

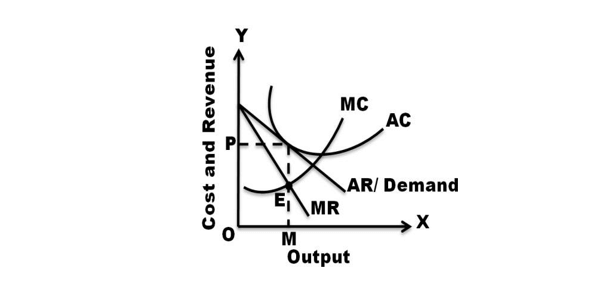

Under monopolistic competition, since different firms produce different varieties of products, different prices for them will be determined in the market depending upon the demand and cost conditions. Each firm will set the price and output of its own product. Here also the profit will be maximized when marginal revenue is equal to marginal cost (MR=MC). The demand curve for the firm in case of monopolistic competition is similar to that of a monopoly.

The degree of elasticity of demand of a firm in monopolistic competition depends upon the extent to which the firm can resort to product differentiation. The greater the ability of the firm to differentiate the product, the less elastic the demand is. The firm’s influence to increase the price depends upon the extent to which it can differentiate the product.

In the short-run, the firm is in equilibrium when marginal revenue equals marginal cost. In the figure, AR is the average revenue curve, MR is the marginal revenue curve, MC is the marginal cost curve, and AC is the average cost curve. MR and MC intersect at point E where output is OM and price is MQ (i.e., OP). Thus, the equilibrium output is OM and the price is MQ or OP. When the price (average revenue) is above average cost, a firm will be making supernormal profit. From the figure, it can be seen that AR is above AC at the equilibrium point. As AR is above AC, this firm is making abnormal profits in the short-run. The abnormal profit per unit is QR, i.e., the difference between AR and AC at the equilibrium point, and the total supernormal profit is OR x OM. This total abnormal profit is represented by the rectangle PQRS. The firm may make supernormal profits in the short-run if it satisfies the following two conditions:

- MR = MC

- AR > AC

More and more firms will enter the market, attracted by the supernormal profits enjoyed by the existing firms in the industry. As a result, competition becomes intense. On one hand, firms will compete with one another for acquiring scarce inputs, pushing up the prices of factor inputs. On the other hand, the entry of several firms will increase the supply in the market, pulling down the selling price of the products. To cope with the competition, firms will have to increase their budget on advertising. The entry of new firms continues until the supernormal profits of the firms are completely eroded and ultimately firms in the industry will earn only normal profits. Those firms that are not able to earn at least normal profits will close down. Thus, in the long-run, every firm in the monopolistic competitive industry will earn only normal profits, which are just sufficient to stay in business. It should be noted that normal profits are part of average costs.

In the long-run, to achieve equilibrium, the firm has to fulfill the following conditions:

- MR = MC

- AR = AC at the equilibrium level of output