Posting to Ledger

All the transactions in a journal are recorded in chronological order. After a certain period, if we want to know whether a particular account is showing a debit or credit balance, it becomes very difficult. So, the ledger is designed to accommodate the various accounts maintained by the trader. It contains the final or permanent record of all the transactions in duly classified form. “A ledger is a book which contains various accounts.” The process of transferring entries from journal to ledger is called “POSTING”.

Posting is the process of entering in the ledger the entries given in the journal. Posting into the ledger is done periodically, may be weekly or fortnightly as per the convenience of the business. The following are the guidelines for posting transactions in the ledger:

1. After the completion of Journal entries, only posting is to be made in the ledger.

2. For each item in the Journal, a separate account is to be opened. Further, for each new item, a new account is to be opened.

3. Depending upon the number of transactions, space for each account is to be determined in the ledger.

4. For each account, there must be a name. This should be written at the top of the table. At the end of the name, the word “Account” is to be added.

5. The debit side of the Journal entry is to be posted on the debit side of the account, by starting with “TO”.

6. The credit side of the Journal entry is to be posted on the credit side of the account, by starting with “BY”.

Proforma for ledger: LEDGER BOOK Account

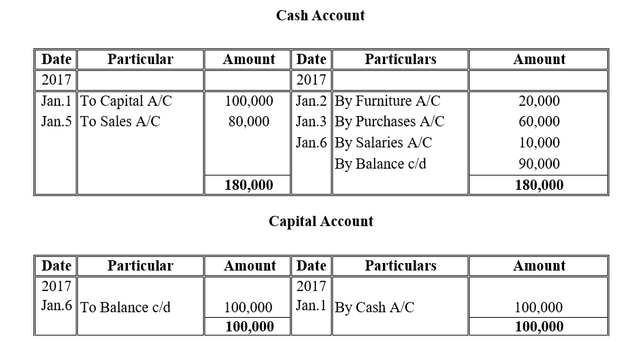

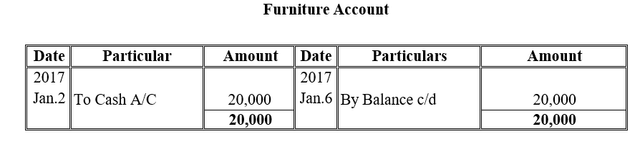

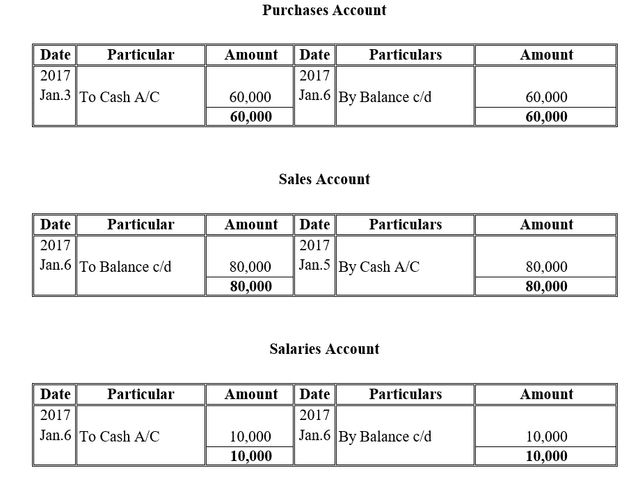

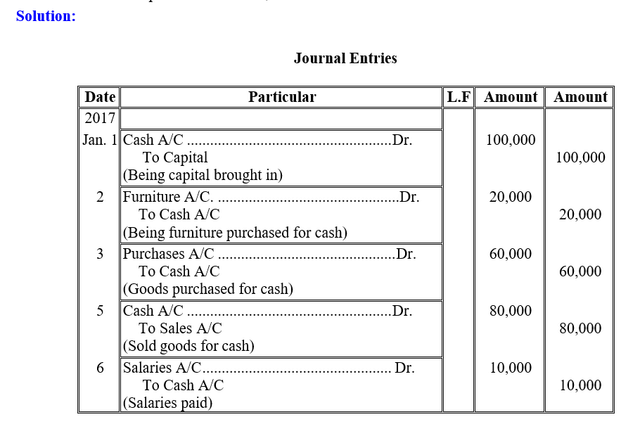

Example

Enter the following transactions in journal and post them into ledger:

2017

Jan 1: Mr. Rameh started business with cash Rs. 100,000

Jan 2: He purchased furniture for Rs. 20,000

Jan 3: He purchased goods for Rs. 60,000

Jan 5: He sold goods for cash Rs. 80,000

Jan 6: He paid salaries Rs. 10,000

Ledger